Patience is a vital tool in financial planning.

As I mentioned in my last post, I want to do more with Faith-based topics in financial planning. As we look again at the Fruits of the Spirit from Galatians 5, let’s focus on patience.

In a world where we can have anything our hearts desire almost instantly, patience is becoming a rare fruit of the Spirit. Normally, when something is rare it becomes valuable. No, we shouldn’t compare these characteristics as we need them all, but if I were to rank them, I would place patience at the top of my list.

Depending on the translation of your Bible, you may see forbearance listed instead of patience in the fruits of the Spirit in Galatians 5:22. I think forbearance is more about being patient with our fellow man, such as when someone needs an extra few days to pay back a loan. Here, I’ll be referring to patience in general because it supports my argument and we need patience more than ever in today’s world.

Dad loved to say, “Patience is a virtue.”

I always loved fishing with my dad. Fishing is a great way to learn patience. Sometimes you go home empty-handed. After all, it’s called fishing and not catching for a reason.

I always loved fishing with my dad. Fishing is a great way to learn patience. Sometimes you go home empty-handed. After all, it’s called fishing and not catching for a reason.

Imagine spending 5 hours outside, sitting quietly, being a buffet for mosquitoes, and not catching anything. You go home and your mom says, “Weren’t you bored being out there so long and not catching anything?” Absolutely not! Those were some of my best days!

I think my dad initially tried to use fishing to teach me patience, but I had no problem sitting there. Where I struggled was being patient waiting for Dad to quit working and take me fishing!

He would say we could go fishing the next day, but never said what time. I would wake up ready to go the next morning, but we rarely ever left before 4:00 in the afternoon. Sometimes I would become so irritated and impatient that I didn’t want to go at all, but I never actually passed up the opportunity to wet a hook.

Patience is a learned behavior that takes time to develop.

The best thing about learning patience is that it teaches you to be, well, PATIENT! Good things normally come to those who wait. Jesus said he was going to prepare a place for us, then He would return (John 14: 1-3). As Christians, we wait patiently for that day, but we don’t just sit around waiting. We work hard, try to accomplish our goals, and live our lives (While trying to introduce as many people to Jesus as possible).

If we can wait patiently for Jesus to return, why can’t we be more patient in our daily lives? We don’t know when He will return, but we know He will and then He will fix everything that is wrong with the world. This may not even happen in our lifetimes, but we don’t complain because we believe it will happen.

Yet we can’t wait three minutes for the streetlight to turn green or for a television show to come back from commercials? Sure, I become impatient too, but with that perspective all I can say is WHAT IS WRONG WITH US?

In the grand scheme of things, these inconveniences are so small. However, we risk our lives just to get to our destination a little bit faster or we have meltdowns because we aren’t entertained for a few moments. It really doesn’t make a lot of sense.

Patience requires commitment.

When my mom was working she had a sign in her office that said, “Poor planning on your part doesn’t create an emergency on my part.”

My fear is that we are doing this with our retirement planning. Things will always come up, but we have to make a commitment to our future. No, we cannot guarantee that we’ll live long enough to make it to retirement. Jesus may come back and we won’t even need those resources, but wouldn’t you like to be prepared?

I get frustrated with the argument that we can’t save for our future because we can barely survive today. Yes, life is hard, but it’s supposed to be. Jesus said, “In the world you will face tribulations, but fear not for I have overcome the world.” (John 16:33)

If everything was perfect, would we be appreciative of our blessings or would we forget our need for Jesus? Nothing goes well for any people who forget about Him. Sometimes it’s actually good to have struggles because it helps us appreciate what we have and can even lead to opportunities.

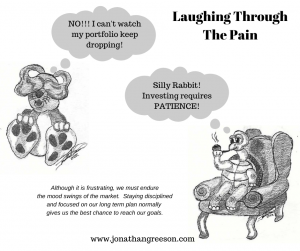

Knowing that life will have its ups and downs should make us more comfortable when the stock market goes through some turmoil. In a time like this we need to be patient. If the markets had no risks, there would be no value to investing.

Furthermore, when the market goes down, there may be opportunities. Similar to when a desirable product is on sale for a lower price, there can be some good deals when the market is going down. Unfortunately, there are no flyers or billboards saying there will be a sale in the stock market, so we have to plan.

Patience helps with investing through financial planning.

The stock market is not a lottery or a get rich quick scheme. It is also not scam where you need to try to outwit the rich or time the market. When we try and “beat the market” we normally do the exact opposite of what we should do. Instead of buying low and selling high, we react to the market by buying high and selling low.

Wayne Gretzky is credited with saying, “Good players go where the puck is, but great players go where it’s going to be.” Let me take that a little further and say to be in a position to play the puck, you must be on the ice at every opportunity, not just at points where you know you will win.

In order to be successful in the market, you don’t time it, you invest in it! When you invest money in a retirement plan you don’t intend to use it until later. Patience is vital here because you’re going to have to endure market movements.

It can be frustrating watching your account balance each day, so I suggest treating your IRA like you do your 401(k).

In your job, you may be able to change the allocation, but you cannot control who manages the 401(k). You can’t change your investment when someone gives you a hot tip or because you believe one wealth manager can manage a downturn better than another. You love your job, so you patiently endure the daily moves of the market and hope to have a decent amount available in retirement.

I firmly believe that a 401(k) is not enough for retirement in the future even with some type of Social Security payment. We need the third option, which is our personal resources. This includes your IRA (Preferably a Roth IRA). If you don’t have one, or want to move it, I can help with that. Send me an email.

Then, we can develop a plan where you can contribute what you can and patiently let your money work for you. I know it’s scary to give up control of your limited resources, but I encourage you to read the Parable of the Talents (Matthew 25). Those who invested were rewarded for their courage and faith, but the one who didn’t was punished.

I’ve written about this before, but here is the question again.

If we believe that God will provide and has an individual plan for us, then doesn’t it make sense that He knows exactly the amount of resources we’ll need in our lifetime? What if those resources, including money, are provided to us in our career and we are expected to use them in the later years when we aren’t able to work?

In financial planning we call this time of life the accumulation phase. If we spend it all “living for the moment” or “living our best life,” then there may not be any resources left for when you can no longer earn an income.

Then we may have to rely on the Government’s help.

As someone who lives with government assistance because of my disability I can honestly say you don’t want to live that way. Yes, I’m glad to receive help and these are great programs that help many people. However, there are restrictions placed on you to enroll in this programs.

As someone who lives with government assistance because of my disability I can honestly say you don’t want to live that way. Yes, I’m glad to receive help and these are great programs that help many people. However, there are restrictions placed on you to enroll in this programs.

It’s hard to really appreciate the value of financial independence until you are punished for trying to earn more. This is why I think it’s so important that we find the balance between enjoying today and preparing for tomorrow. I don’t want you to have to rely on political decisions for the resources needed to live in the future.

By making the sacrifice today of putting money in a retirement account and waiting patiently for the account to grow, we should be in a better position to survive (and maybe even enjoy) our future.

In college one of my economics teachers was talking about peaches, which got my attention because my dad grew them. The professor said that peach farmers could make more money sending their fruit to New York City instead of selling locally. When the peaches are shipped, they are picked early, so they are hard enough to handle the travel. They ripen over that time and look good in the store where the New Yorker purchases them.

The New Yorker believes the peach is good because they don’t know any better. Sure, the peach is ripe and it has some natural sweetness, so it’s not bad. However, locals know it’s not the best either. We want peaches to stay on the tree until we can eat it the moment it’s picked in the orchard. Only then does it have all of the natural sweetness and tenderness that we know and love.

Unfortunately, this is much more work on the farmer. Have you ever tried to raise fruit? It’s a pain in the butt! It’s definitely easier for farmers to send average peaches to New York compared to having orchards full of perfect peaches for the local market.

I’ll gladly wait patiently for local peaches to be available at a roadside stand instead of buying in a store. Watching and waiting for our retirement account to grow is frustrating, but that can make the future rewards much sweeter.

If you’re ready to plan for your future, email me.